How to Design Your Diligence Process for a Flawless SEBI Audit Trail

Your SEBI system audit is in three weeks, and someone just asked, “Can we prove who saw the financial model on March 4th?” You scramble through email threads and shared folders, only to find three versions of the document and no clear access log. That scramble is the real audit failure. And it happened months ago, when the diligence process was set up without traceability in mind.

A flawless SEBI audit trail isn’t something you build right before the auditor walks in. It’s the natural output of a diligence workflow designed around evidence from day one. Merchant bankers and their compliance teams managing IPOs and M&A need a unified process that works across brokers, RIAs, and all other entities involved. This article lays out exactly how to build that workflow: what evidence SEBI expects, a seven-step framework that generates it automatically, and how to keep the deal moving while you do it.

Why “Audit-Trail-Last” Diligence Breaks Under SEBI Scrutiny

Most diligence workflows are set up for speed, not traceability. Files go into shared drives, Q&A happens over WhatsApp and email, and access is granted by forwarding a link. This feels efficient until SEBI asks you to prove what happened.

The problem isn’t carelessness. It’s that generic tools like email and shared drives don’t capture evidence by design. There is no persistent log of who opened a file, no record of which version was reviewed, and no way to prove a counterparty was restricted from a sensitive folder. Trying to reconstruct that evidence at audit time is slow, incomplete, and often impossible.

What “Flawless” Really Means in Practice

Flawless doesn’t mean documenting every single click. It means you can prove who had access to what and when. It means you can show that your controls were in place throughout the deal. And you can retrieve that evidence quickly. This combination of traceability, completeness, and speed is what separates a clean audit from a corrective action notice. It relies on a system designed to provide comprehensive audit trails and granular access controls automatically, which reduces manual evidence collection.

What a SEBI-Ready Audit Trail Must Be Able to Prove

Before designing your process, you need to be clear on what “evidence” means. Auditors are not just checking if documents exist. They are verifying that your controls were active, consistent, and enforceable throughout the transaction.

The 5 Evidence Buckets: Access, Actions, Changes, Decisions, Remediation

Think of your audit evidence in five main categories:

If your workflow can’t produce evidence across all five buckets on demand, you have a gap.

Where Teams Accidentally Lose Evidence (And Don’t Realize It)

The most common evidence losses happen quietly and look like normal work.

Each of these is a potential non-compliance finding. They all stem from normal deal-team behavior in a workflow that wasn’t designed for audits.

The Audit-Trail-First Diligence Framework (7 Steps)

This framework maps each diligence action to the evidence it generates and the audit verification it supports. Use it as your operating system for every deal.

1) Start with an “Auditor-Friendly” Document Map

Before uploading a single file, build a folder structure that an auditor can navigate in minutes.

- [Category]-[Subcategory]-[Document Name]-[YYYY-MM-DD]. No more “final_v2_revised.”

2) Define Roles and Permission Groups Before Uploading a Single File

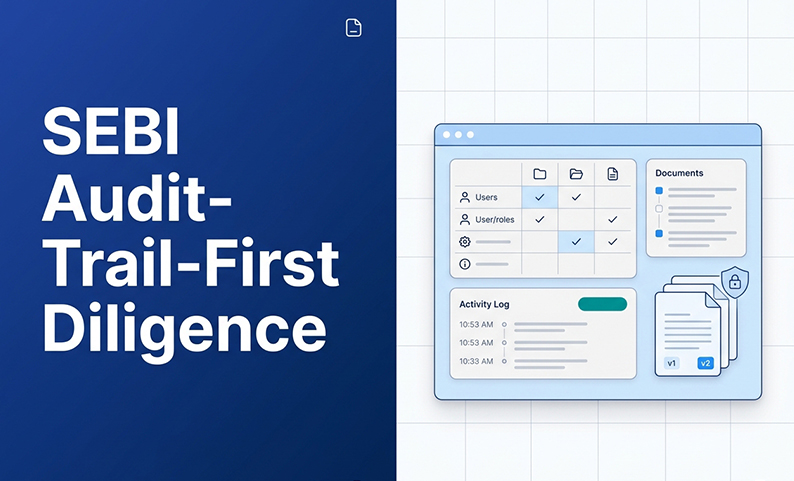

Access chaos is a primary source of SEBI audit findings. The fix is a clean permission architecture from the very start.

DCirrus VDR supports this with folder and file-level permissions, device-level approval using unique device IDs, IP address restrictions, and MFA via SMS, email, or Microsoft Authenticator. Each control strengthens the audit log by documenting access restrictions.

3) Make Every Sensitive Document Traceable by Design

Documents won’t always stay in the VDR. The question is whether you can still trace what happens to them.

- Digital Rights Management (DRM) to restrict printing and copying where allowed.

4) Keep Versions, Approvals, and Replacements Auditable

Version control is about proving the right people approved the right documents at the right time.

5) Move Q&A into a Single System with Full Traceability

Q&A is where deals leak evidence. A response in an email inbox isn’t part of the official document record.

DCirrus VDR’s built-in Q&A forums, secure messaging, automated notifications, and version control keep every clarification, decision, and document update in one auditable place. This removes the need to reconstruct decisions from scattered email chains.

6) Build Continuous Monitoring into the Cadence

A weekly evidence check catches gaps before they become non-compliance findings.

7) Prepare Remediation and Follow-Up Audit Readiness During Diligence

When a gap is found, the record of your corrective action matters as much as the fix itself.

Comparison Table — Three Ways Teams Run Diligence

Suggested visual: A simple line/area chart showing audit prep effort (hours per deal) decreasing as workflow maturity increases from Email → Basic VDR → Audit-Trail-First Diligence. As maturity increases, the “last-minute audit scramble” effort drops toward zero.

Email/Shared Drive vs Basic VDR vs Audit-Trail-First Diligence

| Dimension | Email / Shared Drive | Basic VDR Usage | Audit-Trail-First Diligence |

| Access logs | None | Basic login records | Granular: user, IP, device, timestamp, action |

| Document traceability | File names only | Folder structure, some versioning | Full version history, changelogs, approvals |

| Q&A capture | Scattered email threads | External email or basic comments | Structured, categorized, linked to documents |

| Watermarking | Manual (or none) | Optional per document | Automatic on all views/downloads |

| Permission segregation | Folder sharing (all or nothing) | Role-based, limited granularity | Folder/file-level + device + IP + MFA |

| Audit prep effort | Very high (manual reconstruction) | Medium (some export capability) | Low (on-demand export, pre-organized) |

| Leakage risk | High | Moderate | Low (DRM + watermark + download controls) |

| SEBI NC risk | High | Moderate | Low (continuous monitoring catches gaps early) |

Implementation Guide: Who Owns What and How to Roll This Out Mid-Deal

Knowing what to do is half the problem. Knowing who does it is the other half.

RACI: Deal Lead, Compliance, IT/Security, External Counsel, Auditors

| Task | Deal Lead | Compliance | IT/Security | External Counsel |

| Document map and naming conventions | R | C | I | C |

| Permission groups and provisioning | C | R | R | I |

| Watermarking and DRM configuration | I | C | R | I |

| Version control and approval checkpoints | R | C | I | C |

| Q&A management and SLA tracking | R | C | I | R |

| Weekly evidence checks | C | R | C | I |

| Issue log and remediation tracking | C | R | C | I |

R = Responsible, C = Consulted, I = Informed

The compliance lead is the single internal owner of audit readiness, while deal leads own execution.

Mid-Deal Transition Plan (Minimum Disruption)

Switching from email and shared drives mid-deal is manageable if you do it carefully.

Vendor/Tool Evaluation Questions

Ask these questions to see if a platform can support an audit-trail-first workflow:

Common Failure Modes That Trigger NCs—And How to Catch Them Early

You can prevent common pitfalls from becoming audit findings if you know what to look for.

The “Silent Killers”: Unmanaged Access, Offline Sharing, Missing Approvals, Untracked Q&A

Small gaps often compound into major non-compliance issues. These include granting overly broad access “just in case,” failing to track documents once they are downloaded, skipping formal approval steps on “minor” revisions, and resolving critical questions in unlogged hallway conversations or email threads. The seven-step framework is designed to eliminate these silent killers by making the correct, auditable action the easiest path.

A Lightweight “Weekly Readiness Dashboard”

To stay ahead, track a few key metrics weekly. You don’t need complex software for this. A simple, shared report is all it takes.

Summary and Next Steps: Make Audit Trails a Byproduct, Not a Project

A flawless SEBI audit trail isn’t created by a last-minute scramble. It’s the natural result of a diligence process designed for traceability from day one. When you standardize your document structure, control access, and capture actions in a single system, you make audit readiness a continuous, low-effort byproduct of your daily work. This disciplined approach also makes it far easier to adapt to evolving SEBI circulars and timelines because the core evidence-gathering engine is already in place.

Your First 30-Minute Action: Pick One Deal and Run the 7-Step Gap Scan

Don’t try to boil the ocean. Pick one active or recent transaction and use the 7-step framework in this article as a checklist. Where did you lose evidence? Where were the controls weak? This simple gap analysis will give you the business case and a clear starting point for building your audit-trail-first diligence process.

FAQ

Want a diligence workflow that produces audit-ready logs automatically?

DCirrus VDR helps you enforce a SEBI-ready diligence process with granular permissions, built-in Q&A, dynamic watermarking, and one-click audit trail exports. Book a free demo to see how you can make your next audit flawless by design.

Latest Posts